By: Jeff Anderson, CFA

| Close | Weekly return | YTD return | |

| S&P 500 | 4,271.78 | -2.75% | -10.37% |

| Nasdaq Composite | 12,839.29 | -3.83% | -17.93% |

| Russell 2,000 | 1,940.66 | -3.21% | -13.57% |

| Crude Oil | $101.22 | -5.0% | 34.13% |

| US Treasury 10yr Yield | 2.90% | 1.3% | 91.52% |

Source: Wall St. Journal

Market Wrap:

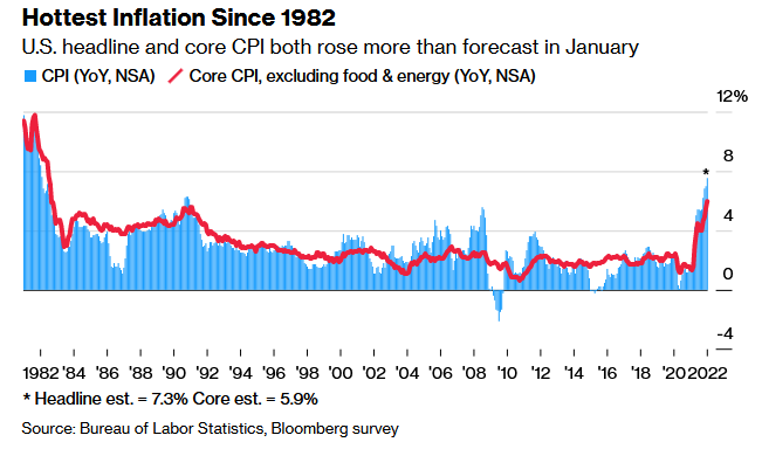

The major indices suffered another week of losses as investors digested Fed Governor Powell’s comments earlier this week. Mr. Powell is committed to fighting inflation and the next meeting on rates in Mid-May looks like a 0.5% increase in interest rates will be the decision. There are even rumblings of a potential 0.75% hike. Investors worry that an aggressive interest rate hike stance will slow economic growth and hurtle the US into a recession. No one knows definitively if a recession will happen, but the market is acting like it is a foregone conclusion. The economy moves in cycles. Recessions are a part of that cycle. That is undeniable. While the market continues to fret over these fears, the US economy is in good shape. Corporate earnings have been, for the majority, strong. The consumer continues to spend and has elevated savings levels. Airlines had a great first quarter. Despite higher air fares, people are taking to the skies. Steel companies are doing well. Tesla cannot keep up with demand. Will this be the case in 6 to 9 months? It is anybody’s guess. Goldman Sachs said this week that there is now a 35% of a recession in the US within the next two years. To me, that is a useless piece of information. That’s just fence-sitting. As markets fall, they do become cheaper. Maybe earnings will fall, or slow at a faster pace than anticipated, but this is cyclical, not necessarily secular. The S&P 500 is trading below 18 times this year’s estimated earnings. That is near its historical average. It is less expensive than it has been for years. Looking out five years from now, will corporate America be earning more than today? Odds are they will. There may be a pullback or two along the way, but it is a reasonable bet. Famed investor Warren Buffet has always maintained that the US economy is much more resilient than many people think and that, over the long-term, investing in corporate America pays off. Being able to ignore the short-term market fluctuations and being able to invest during bear markets gives the investor much better odds at reaching their retirement goals.

“Bonds don’t work anymore”

I’ve heard this a few times recently. The first quarter of this year saw both stocks and bonds lose value. That is rare. Given the inflationary environment we’re in, it’s not terribly surprising. Bonds move in the opposite direction of interest rates. The longer the maturity, the more dramatic the price declines when interest rates increase. Longer maturity bonds are more sensitive to changes in interest rates. At some point, rate hikes will slow, or stop, and bonds that have lower coupons (the “interest rate” part of the bond) will mature and can be reinvested at higher interest rates. Having yields too low isn’t healthy long-term. The reason they were low was because of the pandemic. The fear was deflation, not inflation. As the Fed raises rates, inflation will start to come down. Add in improvements in the global supply chain and an end to the war in the Ukraine and we could see inflation well below 5%, and even closer to 3%. At that point, rates will stop going up and it will give the Fed the tools necessary to tackle the next recession or, God forbid, another pandemic-like event. Having rates stuck below 2% coming into a recession leaves little room for the Fed to help. Restoring balance after the global pandemic is what’s important.

So, are bonds still a good investment? Yes. They are a vital component of a well-diversified portfolio. They should return to providing a ballast to the equity portion of a portfolio. They should offer more attractive income returns, and they should be less volatile than equities. Judging any asset class over a short period is a poor way to think about your portfolio. Over the short-term, it’s the uncertainty that worries investors. As we have said many times in the past, there is no such thing as certainty. The world is uncertain. Embracing uncertainty is paramount. Put away the foggy crystal ball. Remember that you have a plan that lays out a path to reaching your financial goals.