By: Jeff Anderson, CFA

This Week: Volatility in the bond and equity markets continued this week. The S&P 500 clawed back over half of its 9.2% sell-off in January early this week, before selling off again. We are still above the January 27th lows. Geopolitical risks, pending interest rate hikes, and elevated inflation levels were at the forefront of this week’s market headlines. As we discussed in today’s podcast, there’s always something to worry about in the short-term, but, as time goes by, those worries become less relevant given the world’s adjustments.

Crude Oil closed at $93.89 per barrel, up 2.1% for the week. The latest CPI release coupled with a more imminent threat of Russia invading the Ukraine, pushed oil higher.

| Close | Weekly return | YTD return | |

| S&P 500 | 4,418.64 | -1.82% | -7.29% |

| Nasdaq | 13,791.15 | -2.18% | -11.85% |

| Russell 2,000 | 2,030.15 | 1.39% | -9.58% |

| US Treasury 10yr Yield | 1.918% | 0.7% |

Source: Wall St. Journal

Your Recently Purchased Car Might Be Worth More Than When You Bought It:

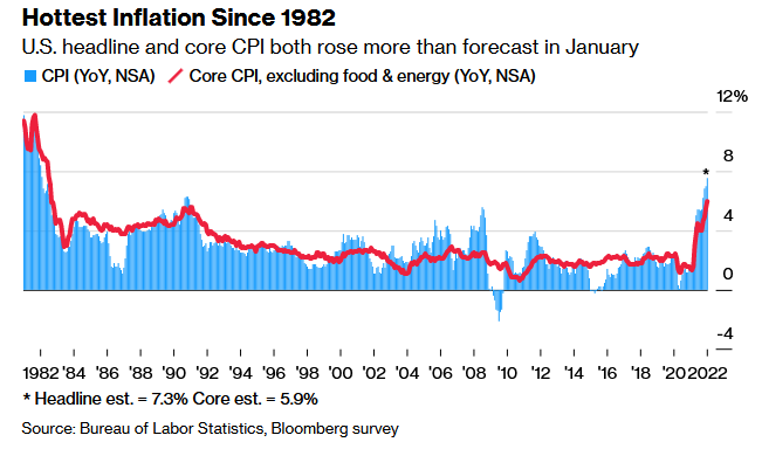

The latest release on the Consumer Price Index showed CPI up 7.5% for the past 12 months, ending January 2022. In the release, used cars and trucks were up a staggering 40.5%. There just are not enough cars or trucks. Supply-chain issues, notably around semiconductor chips, has really put a dent in auto production. Dealer inventories are at historic low levels. Automobiles are historically a depreciating asset, but, thanks to supply-chain issues, your car has increased in value. This is another example of the disruption happening as the global economy is still trying to adjust itself after the pandemic- related shut down.

Large Investment Bank Believes that the Fed Will Hike Rates 7 times this year:

Goldman Sachs stepped up its forecast for US rate hikes for 2022. Just last week, they were calling for five hikes. Now they believe, based on the recent CPI data, that seven will be required. Although nowhere near the inflation rates in the 1970’s, inflation is elevated relative to the past 40 years. The Fed is committed to fighting inflation but will have to balance a high-wire act of tamping down inflation without killing the economy. Credit markets are already adjusting, with the yield on the US 2-year government note up to 1.6% vs 0.12% a year ago. Many of us have never experienced a high-inflation environment. If/when supply-chain pressures ease, it should help minimize the need for such an aggressive rate hike path. We likely will not know until the second half of this year. The Fed, under Governor Powell, has shown itself to be able to change course when the data changes. Longer- dated US government bond yields are not moving up as quickly as the shorter- dated bonds, implying that rate hikes are more likely to slow the economy. As short duration bonds mature, the proceeds can be re-invested at higher rates. At least that is a positive.