By Jeff Anderson, CFA

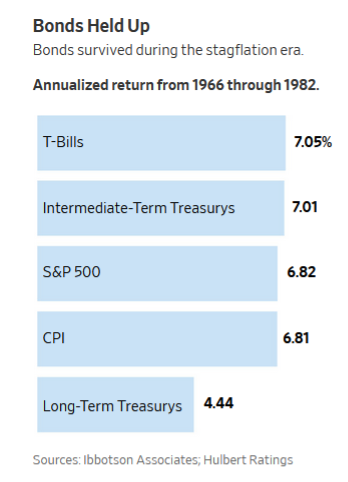

US equities were lower in September, with the S&P 500 logging its first decline since January and its worst month since September 2020. The S&P 500 declined 4.76% for the month. The yield on the US Treasury 10-year note climbed 19.8% to 1.487% and is back to where it was just prior to the onset of the Global pandemic in early 2020. Oil rallied 7.65% for the month to close at $75.12 per barrel. Bonds can perform well in a rising interest rate, low growth environment if the bond portfolio is laddered – portfolios of bonds with a fixed duration target. Most bond mutual funds and ETFs construct their portfolios to maintain a fairly constant average duration which is accomplished by constantly reinvesting in longer-dated bonds from the proceeds of matured bonds. The higher yields of those newly purchased bonds eventually will make up for the capital losses incurred by previously owned bonds.

Employment Data Delayed (no need to be alarmed)

The US monthly employment report typically comes out the first Friday of the month. For October, it won’t be released until the 8th (next Friday). Consensus for non-farm payrolls is looking for growth of 513,000 in September, while the unemployment rate will drop to 5.0% from 5.2%. First Trust’s economists believe that the consensus may be overlooking the fact that the national system of overly generous unemployment benefits due to COVID-19 ran out on Labor Day weekend. “Many unemployed who had previously been getting payments in excess of what they could have earned while working are no longer able to do so”. Couple that with kids going back to in-school learning, the motivation for people to get back to work are the strongest in months. With employers struggling to hire employees and/or pay more in wages, this may come as a nice surprise.

Prices to The Moon

Much of the increase in rents is attributable to the pandemic and the rental vacancy spike and eviction moratorium enacted by the federal government. Regardless, the Dallas Federal Reserve predicts that the official rent index from the Bureau of Labor Statistics will increase 6.9% by year-end 20-23, which would be the highest in more than 30 years. Despite the ongoing debate surrounding an increase in inflation being permanent or transitory, certain sectors of the economy continue to eat into the wallets of the US household.