By: Dave Chenet, CFA, CAIA®

| Close | Weekly return | YTD return | |

| S&P 500 | 4,109.31 | 3.48% | 7.03% |

| Nasdaq Composite | 12,221.91 | 3.37% | 16.77% |

| Russell 2,000 | 1,802.48 | 3.88% | 2.35% |

| Crude Oil | 75.67 | 6.55% | -5.68% |

| US Treasury 10yr Yield | 3.49% |

Source: YCharts, Yahoo! Finance, WSJ

Market Recap

March finished on a positive note, with the S&P 500 advancing 3.5% on the month and 6.4% above the March 10th lows. Easing concern about the banking sector and slowing inflation gave rise to the hope that the Fed will achieve a ‘soft landing’ – bringing inflation down towards its 2% target without pushing the economy into outright recession. Under the hood, gains in tech and communication services offset losses in financials and real estate. Regionally, Emerging Markets outperformed developed markets and bonds finished the month higher as treasury yields fell.

On a quarterly basis, both stocks and bonds were broadly higher. European markets were the best performer for the second consecutive quarter and have significantly outpaced US stocks over that period as easing recessionary fears, hope of peaking inflation and very low valuations, and a falling US dollar vs the Euro all supported European stocks (in US dollar terms).

Looking ahead, we are two weeks away from the start of a pivotal earnings season. Investors will keep a keen eye on companies’ expectations around revenue growth and the impact of higher rates on corporate profits.

What We’re Reading:

Mohammed El-Erian: What happens in the Banking Sector Won’t Stay There

Richmond Fed President Barker: The Need to Be Nimble

Federal Reserve: Senior Loan Officer Opinion Survey on Bank Lending Practices

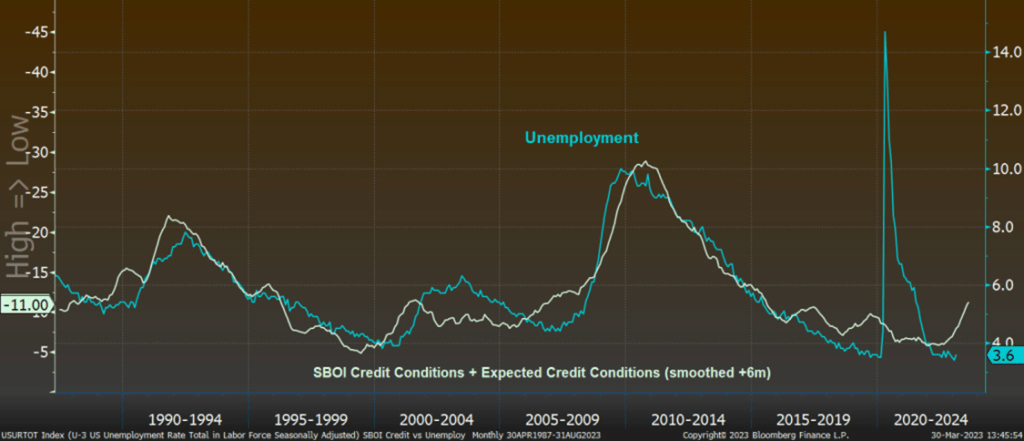

Chart of the Week:

While the actions from the US Treasury to quell the banking turmoil of the last few weeks may have alleviated the immediate pressure on banks, the economic impact may be yet in its early stages. Data suggests that banks are tightening lending standards, which is a leading indicator for the health of the labor market. Should credit conditions remain tight, the likelihood of recession is materially higher.