By: Dave Chenet, CFA, CAIA

| Close | Weekly return | YTD return | |

| S&P 500 | 4,205.45 | 0.32% | 9.53% |

| Nasdaq Composite | 12,975.69 | 2.51% | 23.97% |

| Russell 2,000 | 1,773.02 | 0% | 1.00% |

| Crude Oil | 72.77 | 3.13% | -9.21% |

| US Treasury 10yr Yield | 3.81% |

Source: YCharts, Yahoo! Finance, WSJ

Market Recap: Have We Already Entered Recession and Should We Care?

The wall street aphorism that the market is not the economy has rung true so far this year. US Large Cap stocks are up almost 10% through the first five months of the year, powered higher by the high-flying tech stocks, despite signs that the ongoing unwind of fiscal and monetary stimulus is slowing growth and leading to pockets of stress in the markets.

The minutes released this week from the Federal Reserve’s May meeting showed the central bank’s delicate decision: continue to raise rates to fight inflation that remains persistently high and risk tipping the economy into recession or refrain from further hikes to stabilize the economy but risk inflation reaccelerating. Economically, manufacturing data, corporate profits, constrained bank lending, rising consumer debt/delinquencies and higher borrowing costs all point to slowing growth. Eventually the slowing growth picture will reduce demand-side pressure on inflation and will allow the Fed to lower interest rates to more accommodative levels, however, a recession would likely also lead to lower corporate earnings and lower stock prices in the short-term.

Disciplined investors may be well-served by paying close attention to the economic data and prepare their portfolio for rockier times ahead. To quote another aphorism (or maybe a JFK quote): the time to repair the roof is when the sun is shining.

What We’re Reading:

Strong US consumer spending, inflation readings put Fed in tough spot

Morningstar: What’s the Best-Performing Asset Type During a Recession

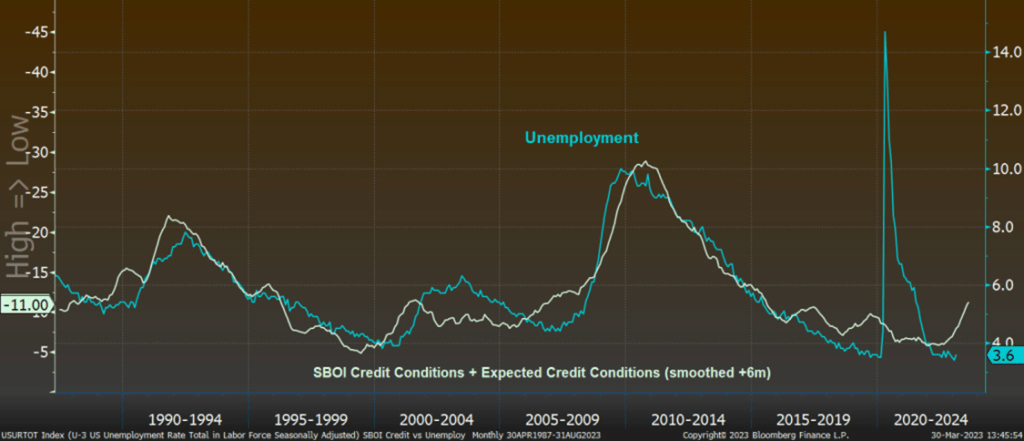

Chart of the Week:

The Bureau of Economic Analysis (BEA) compiles two measurements of economic output – Gross Domestic Product (GDP) and Gross Domestic Income (GDI). In theory, these two measurements should be equivalent – they both track the aggregate output of the US economy. In the short term, however, the two can deviate. Economists argue that the GDI might more quickly predict recession as its inputs may be more timely than the output-focused GDP components. Today, the GDI (blue line in the chart above) is signaling that we may have entered a recession – despite a modest pickup in the GDP estimate.