By: Dave Chenet, CFA, CAIA

| Close | Weekly return | YTD return | |

| S&P 500 | 4,193.20 | 1.64% | 9.18% |

| Nasdaq Composite | 12,664.30 | 3.04% | 20.94% |

| Russell 2,000 | 1,773.72 | 1.91% | 0.95% |

| Crude Oil | 71.77 | 2.72% | -10.58% |

| US Treasury 10yr Yield | 3.69% |

Source: YCharts, Yahoo! Finance, WSJ

Market Recap: Is the Tech Trade Back?

After leading the markets to the downside last year, US large-cap stocks have been the best performer year-to-date. The equal-weighted S&P 500 index is +1.14% for the year vs. a +9.44% rally for the market-cap weighted S&P 500 index. On a single stock basis, Nividia and Meta (formerly Facebook) have more than doubled in value over the course of the year. Two main factors are responsible for the rally in tech shares:

- The AI Boom: investors have been enamored with companies that may be exposed to the wave on Artificial Intelligence (AI) applications. An analysis by Societe Generale finds that removing the 20 stocks most widely owned by AI-focused funds would reduce the S&P 500 performance by roughly 10% year-to-date).

- Expectations of an Upcoming Fed Pivot: Despite efforts from Chairman Powell and other Fed presidents to convince the markets that the Fed may indeed continue to hike rates if inflation does not return to the 2% level, the market expects central bankers will soon be cutting rates. Current market pricing reflects the assumption that the Fed will cut short-term borrowing costs by 0.5% by year-end. This shift to (more) accommodative monetary policy will likely benefit the interest-rate sensitive technology sector.

Investors may be well served to closely examine their risk tolerance and time horizon before chasing after returns in tech stocks, however. We highlight a few factors which could derail the rally:

- Stagflation: slowing growth (whether an official recession or not) combined with persistently sticky inflation will both challenge earnings for tech stocks and valuations. The Fed may be disinclined to acquiesce to the market’s desire for lower rates and the lofty valuations supporting the tech rally may be forced to moderate.

- Valuations: investors must not only consider the quality of the companies that they own, but also the price they pay to own those companies. U.S. “Mega-Cap” stocks (the eight stocks that currently represent almost 25% of the market cap of the S&P 500) are trading at near-record valuations relative to the remaining 492 stocks in the index.

As always, we encourage investors to maintain portfolios that cater to their unique investment time horizon and risk profile. In the long-term, a disciplined process which focuses on risk management and diversification leads to superior results.

What We’re Reading:

Professor Jeremy Siegel: Summarizing, I Remain Cautious On the Markets

Natixis: Why Everyone’s Talking About…Stagflation

Reuters: Artificial intelligence gives real boost to U.S. stock market

BofA Strategist Says Sell US Stocks as AI Seen Forming a Bubble

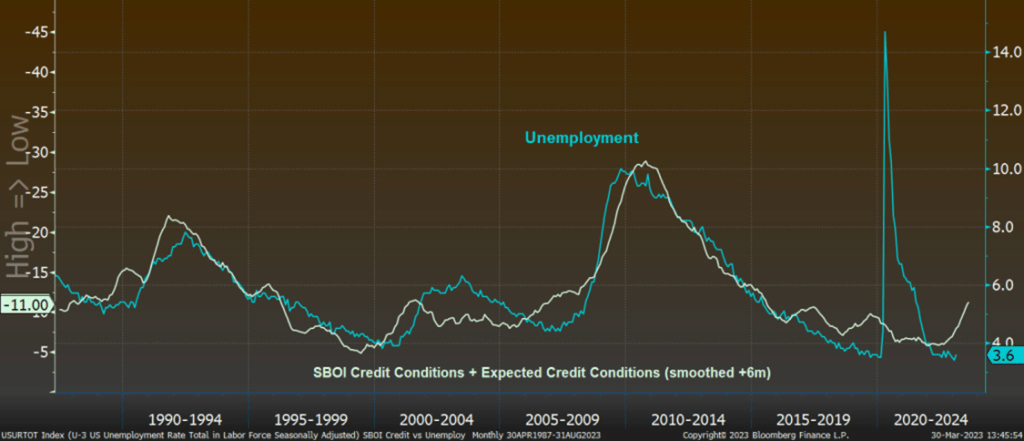

Chart of the Week: