By: Dave Chenet, CFA, CAIA

| Close | Weekly return | YTD return | |

| S&P 500 | 4,124.04 | -0.29% | 7.41% |

| Nasdaq Composite | 12,284.74 | 0.40% | 17.37% |

| Russell 2,000 | 1,740.85 | -0.99% | -0.94% |

| Crude Oil | 70.02 | -1.43% | -12.62% |

| US Treasury 10yr Yield | 3.46% |

Source: YCharts, Yahoo! Finance, WSJ

Market Recap

Despite inflation reports which showed the pace of inflation continues to moderate – both as measured by the Consumer Price Index and the Producer Price Index, markets finished the week lower, weighed down by little progress towards resolving the US debt ceiling. Should congress fail to reach a debt ceiling agreement, the Brookings Institute estimates that the treasury could continue to make interest payments on government debt but would have to cut other outlays by 25%. [1]Lower government spending would slow economic growth and borrowers may require a higher interest rate to lend to the government, thus leading to lower bond prices and lower stock market valuations. Lower asset prices and higher borrowing costs would lower consumer and business confidence. In an economy that many believe may already be on the precipice of recession, failure to reach an agreement would certainly increase recessionary risk. Even if a deal is reached, the economy would not be out of the woods. A deal would likely include spending cuts and act as a tightening of fiscal policy – at a point in time when the Fed has just raised borrowing costs and continues its $95b/month reduction in the size of its balance sheet. Policymakers face a significant challenge – continue fiscal and monetary accommodation to support current growth but risk inflation and lack of progress towards containing ballooning deficits and levels of government debt. Regardless of the outcome, current low levels of market volatility may prove to be overly complacent.

What We’re Reading:

CBO: Update to Budget Outlook 2023 to 2033

FT: US fiscal alarm bells are drowning out a deeper problem

WSJ: Druckenmiller Warns of Risk of US Hard Landing

CNBC: Jamie Dimon warns panic will overtake markets as U.S. approaches debt default

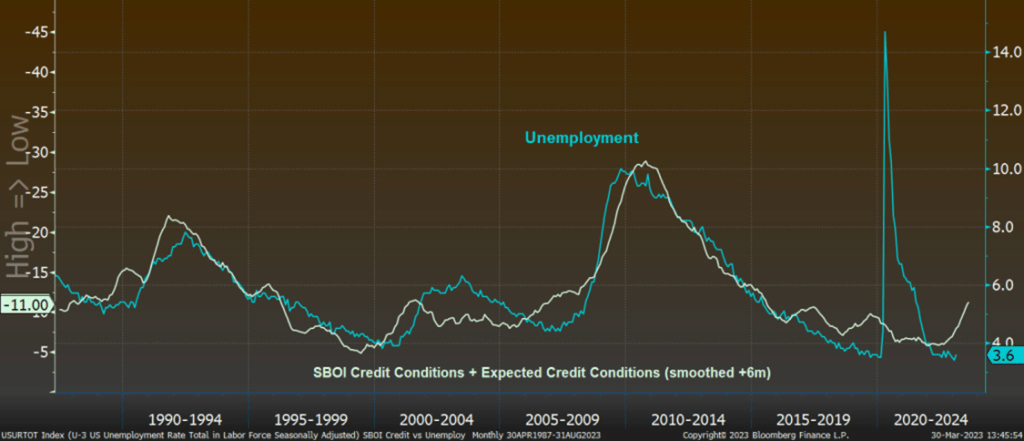

Chart of the Week:

The Consumer Price Index continued to moderate in April yet remains above the Federal Reserve’s 2% mandate. As reflected in the chart above, goods inflation has moderated from the COVID-related supply chain issues, yet services inflation remains high. Core Services inflation will likely continue to moderate (housing and wage growth tend to be leading indicators), yet we believe that it is likely inflation will remain above the level in which the Federal Reserve is likely to cut interest rates.

[1] https://www.brookings.edu/2023/04/24/how-worried-should-we-be-if-the-debt-ceiling-isnt-lifted/#:~:text=choices%20policymakers%20legislated.%E2%80%9D-,If%20the%20debt%20ceiling%20binds%2C%20and%20the%20U.S.%20Treasury%20does,event%20would%20surely%20be%20negative.